Our Good Beta portfolio sourced from Goldman Sachs Asset Administration helps meet the desire of our prospects who’re prepared to tackle extra dangers to doubtlessly outperform a market capitalization technique.

The Goldman Sachs Good Beta portfolio technique displays the identical underlying rules which have all the time guided the core Betterment portfolio technique—investing in a globally diversified portfolio of shares and bonds. The distinction is that the Goldman Sachs Good Beta portfolio technique seeks increased returns by transferring away from market capitalization weightings in and throughout fairness asset courses.

What is a great beta portfolio technique?

Portfolio methods are sometimes described as both passive or energetic. Most index funds and exchange-traded funds (ETFs) are categorized as “passive” as a result of they observe the returns of the underlying market based mostly on asset class. Against this, many mutual funds or hedge fund methods are thought of “energetic” as a result of an advisor or fund supervisor is actively shopping for and promoting particular securities to try to beat their benchmark index. The result’s a dichotomy wherein a portfolio will get labeled as passive or energetic, and traders infer potential efficiency and danger based mostly on that label.

In actuality, portfolio methods reside inside a aircraft the place passive and energetic are simply two cardinal instructions. Good beta funds, like those that had been chosen for this portfolio, search to attain their efficiency by falling someplace in between excessive passive and energetic, utilizing a set of traits, referred to as “elements,” with an goal of outperformance whereas managing danger. The portfolio technique additionally incorporates different passive funds to attain applicable diversification.

This various method can also be the rationale for the title “sensible beta.” An analyst evaluating typical portfolio methods normally operates by assessing beta, which measures the sensitivity of the safety to the general market. In creating a wise beta method, the efficiency of the general market is seen as simply certainly one of many elements that impacts returns. By figuring out a variety of things that will drive return potential, we search the potential to outperform the market in the long run whereas managing cheap danger.

Once we develop and choose new portfolio methods at Betterment, we function utilizing 5 core rules of investing:

- Personalised planning

- A stability of value and worth

- Diversification

- Tax optimization

- Behavioral self-discipline

The Goldman Sachs Good Beta portfolio technique aligns with all 5 of those rules, however the technique configures value, worth, and diversification differently than Betterment’s Core portfolio. With the intention to pursue increased general return potential, the sensible beta technique provides extra systematic danger elements which can be summarized within the subsequent part.

Moreover, the technique seeks to attain world diversification throughout shares and bonds whereas overweighting particular exposures to securities which might not be included in Betterment’s Core portfolio. In the meantime, with the sensible beta portfolio, we’re in a position to proceed delivering all of Betterment’s tax-efficiency options, corresponding to tax loss harvesting and Tax Coordination.

Investing in sensible beta methods has historically been dearer than a pure market cap-weighted portfolio. Whereas the Goldman Sachs Good Beta portfolio technique has a far decrease value than the trade common, it’s barely dearer than the core Betterment portfolio technique.

As a result of a wise beta portfolio incorporates using extra systematic danger elements, we usually solely advocate this portfolio for traders who’ve a excessive danger tolerance and plan to save lots of for the long run.

Which “elements” drive the Goldman Sachs Good Beta portfolio technique?

Components are the variables that drive efficiency and danger in a wise beta portfolio technique. Should you consider danger because the forex you spend to attain potential returns, elements are what decide the underlying worth of that forex.

We are able to dissect a portfolio’s return right into a linear mixture of things. In tutorial literature and practitioner analysis (Analysis Associates, AQR), elements have been proven to drive historic returns. These analyses type the spine of our recommendation for utilizing the sensible beta portfolio technique.

Components mirror economically intuitive causes and behavioral biases of traders in combination, all of which have been properly studied in tutorial literature. Many of the fairness ETFs used on this portfolio are Goldman Sachs ActiveBetaTM, that are Goldman Sach’s factor-based sensible beta fairness funds. Shares are scored in keeping with 4 elements the place the best scoring corporations have higher weighting. The weights are then constrained to be in-line with the market. These elements embody:

Good Worth

When an organization has strong earnings (after-tax internet revenue), however has a comparatively low worth (i.e., there’s a comparatively low demand by the universe of traders), its inventory is taken into account to have good worth. Allocating to shares based mostly on this issue offers traders publicity to corporations which have excessive progress potential however have been ignored by different traders.

Excessive High quality

Excessive-quality corporations exhibit sustainable profitability over time. By investing based mostly on this issue, the portfolio consists of publicity to corporations with robust fundamentals (e.g., robust and secure income and earnings) and potential for constant returns.

Low Volatility

Shares with low volatility are inclined to keep away from excessive swings up or down in worth. What could seem counterintuitive is that these shares additionally are inclined to have increased returns than excessive volatility shares. That is acknowledged as a persistent anomaly amongst tutorial researchers as a result of the upper the volatility of the asset, the upper its return needs to be (in keeping with normal monetary principle). Low-volatility shares are sometimes ignored by traders, as they normally don’t enhance in worth considerably when the general market is trending increased. In distinction, traders appear to have a scientific desire for high-volatility shares based mostly on the information and, consequently, the demand will increase these shares’ costs and subsequently reduces their future returns.

Sturdy Momentum

Shares with robust momentum have not too long ago been trending strongly upward in worth. It’s properly documented that shares are inclined to pattern for a while, and investing in a lot of these shares permits you to benefit from these traits. It’s vital to outline the momentum issue with precision since securities also can exhibit reversion to the imply—which means that “what goes up should come down.”

How can these elements result in future outperformance?

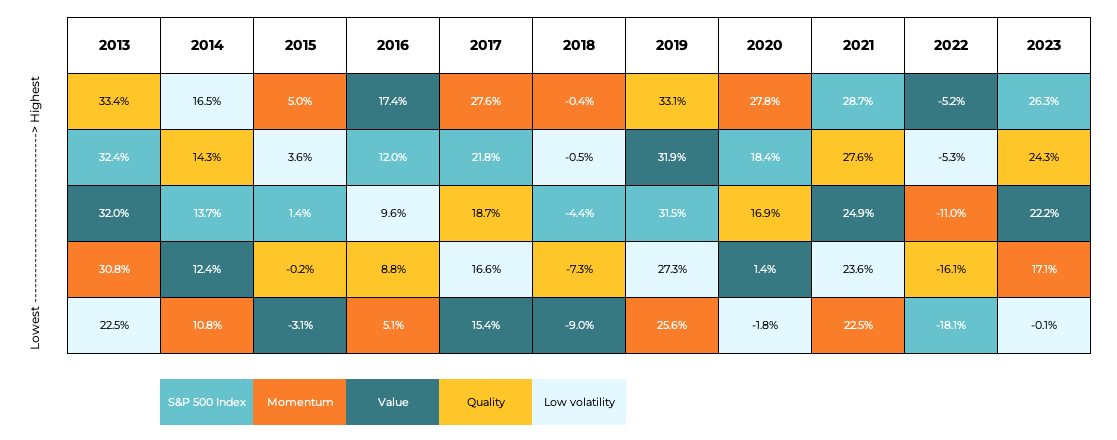

In particular phrases, the elements that drive the sensible beta portfolio technique—whereas having various efficiency year-to-year relative to their market cap benchmark—have potential to outperform their respective benchmarks when mixed. You may see an instance of this within the chart of yearly issue returns for US massive cap shares beneath. You’ll see that the rating of the 4 issue indexes varies over time, rotating outperformance over the S&P 500 Index in almost all the years.

Efficiency Rating of Good Beta Indices vs. S&P 500

Benchmark efficiency info relies on annual returns information from Bloomberg as of January 2013 to December 2023.

Efficiency is offered for illustrative functions solely, and the issue returns it references usually are not essentially the identical issue returns within the Goldman Sachs Good Beta portfolio technique. For every year, now we have ranked the annual efficiency of every issue alongside the S&P 500 as a comparability. The returns for Momentum, High quality, Worth and Low volatility are calculated from the S&P 500 Momentum Complete Return Index, S&P 500 High quality Complete Return Index, S&P 500 Worth Complete Return Index, and S&P Low-volatility Complete Return Index, respectively. This calculation was not offered by Goldman Sachs Asset Administration and doesn’t mirror or predict future efficiency. Furthermore, this evaluation doesn’t embody charges, liquidity, and different prices related to truly holding a portfolio based mostly on these actual indexes that will decrease returns of the portfolio. Previous efficiency is just not indicative of future outcomes. You can not make investments instantly within the index. Content material is supposed for instructional functions and never meant to be taken as recommendation or a advice for any particular funding product or technique.

Why spend money on a wise beta portfolio?

As we’ve defined above, we usually solely advise utilizing Betterment’s selection sensible beta technique in case you’re in search of a extra tactical technique that seeks to outperform a market-cap portfolio technique in the long run regardless of potential intervals of underperformance.

For traders who fall into such a situation, our evaluation, supported by tutorial and practitioner literature, reveals that the 4 elements above might present increased return potential than a portfolio that makes use of market weighting as its solely issue. Whereas every issue weighted within the sensible beta portfolio technique has particular related dangers, a few of these dangers have low or detrimental correlation, which permit for the portfolio design to offset constituent dangers and management the general portfolio danger.

In fact, these dangers and correlations are based mostly on historic evaluation, and no advisor might assure their outlook for the long run. An investor who elects the Goldman Sachs Good Beta portfolio technique ought to perceive that the potential losses of this technique will be higher than these of market benchmarks. Within the 12 months of the dot-com collapse of 2000, for instance, when the S&P 500 dropped by 10%, the S&P 500 Momentum Index misplaced 21%.

Given the systematic dangers concerned, we imagine the proof that reveals that sensible beta elements might result in increased anticipated return potential relative to market cap benchmarks, and thus, we’re proud to supply the portfolio for patrons with lengthy investing horizons.