Tens of millions of American householders would love to maneuver — if they may pack up the mortgage rate of interest they locked in at beneath 4 p.c.

“We hate the world we moved to however can’t justify transferring once more resulting from mortgage charges,” says Ben Younger, who purchased in 2021 at a 2.25 mortgage rate of interest.

The post-COVID fee crater noticed hundreds of thousands of mortgages written or refinanced at traditionally low rates of interest. Owners holding onto that unusually low rate of interest shall be exhausting to dislodge from their present digs. Staying put usually is sensible for particular person households, at the very least financially, however each housing markets and labor allocation are struggling in consequence.

Charges for 30-year mortgages stay properly beneath historic averages, however they’ve nearly doubled up to now three years, proper alongside the Federal Reserve’s rates of interest. The psychological influence of that sticker shock is important. After underestimating the inflationary injury its post-pandemic unfastened cash would generate, the Fed overcorrected with traditionally fast financial tightening, elevating charges 11 instances since spring 2022. The common rate of interest on a 30-year fastened mortgage inched above six p.c in September 2022 and has stayed there. Anybody who locked in a low fee then is pondering twice about giving it up now.

Insurance coverage, property taxes, and value of residing all influence month-to-month bills for householders, and in some instances dwarf the rate of interest differential. However for a lot of, and positively psychologically, giving up a assured low mortgage fee is tough.

David and Sarah Veksler welcomed a 3rd little one this 12 months, however upgrading their house in Denver feels daunting. “Undoubtedly feeling caught right here,” he instructed me. “We’ve a brand new child boy and he’s ready for charges to go down earlier than he can get his personal room. He’ll need to share along with his sisters till then.”

Individually rational selections, in combination, are inflicting an enormous drawback. Even when they didn’t purchase, hundreds of thousands of house owners refinanced in the course of the low-rate years. By spring of 2022, 92.8 p.c of house owners had a mortgage fee beneath six p.c. Six in ten householders nonetheless have a mortgage beneath 4 p.c.

Mounted-rate mortgages are literally adjustable, because of the prepared availability of refinancing choices, however solely in a single course. Debtors refinance to decrease their funds, so fee changes are nearly solely downward. When a purchaser refinances, typically talking, the brand new financial institution points a brand new mortgage and pays off the unique mortgage. The unique lender receives again the principal to lend at 7 p.c, as an alternative of ready for a 30-year mortgage to trickle in on the now-paltry 2.8 p.c. As with different voluntary transactions, all events profit.

A low mortgage fee is extremely fascinating, and non-transferable. As soon as “locked in,” a relatively low mortgage fee capabilities as an emotional and financial anchor. Owners are much less more likely to step up the property ladder (vacating their starter house for a bigger one, or a extra fascinating college district), and in addition much less more likely to downsize and transfer on when their wants change. Each the provision (present houses getting into the market) and the demand (individuals trying to find a brand new one) are suppressed by mortgage fee lock-in. The property market stagnates.

This helps clarify why, as of August 2024, the stock of houses on the market within the US stays 38 p.c off its July 2016 peak and 26 p.c beneath the place it was in August 2019.

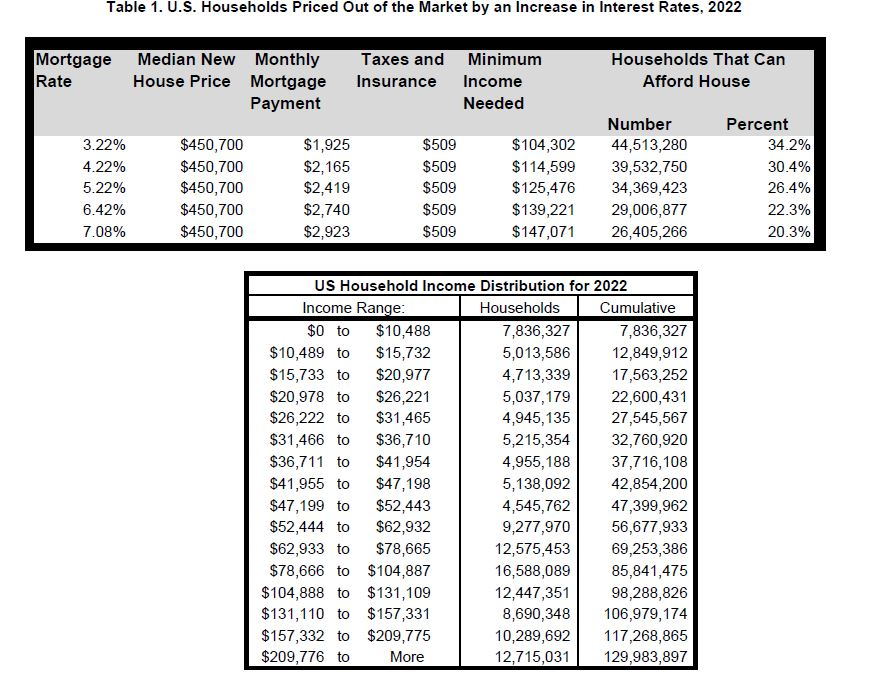

How excessive are the prices of mortgage lock-in? In accordance with analysis by economists Jack Liebersohn and Jesse Rothstein, a 2.7-percentage-point fee hole between locked in and prevailing rates of interest raises the common mortgage stability – the ‘value’ of transferring – by $49,400. Na Zhao, economist with the Nationwide Affiliation of Residence Builders, discovered {that a} rise in prevailing mortgage charges of 100 foundation factors will increase the annual revenue required to qualify for a mortgage by $10,000. Every such bump (from a 4.0 rate of interest to five.0, or 5.5 to six.5) “costs roughly 5 million extra households out of the marketplace for a house on the similar or related value degree.” Only one in 5 American households earns sufficient to qualify for median-priced houses at seven-percent curiosity.

In a turbulent financial time, transferring presents a serious price that may be averted solely by driving out at the very least one other few years at a locked-in pandemic fire-sale fee. Owners dealing with these incentives usually tend to keep put.

Knowledge verify mobility declines as mortgage charges rise. Liebersohn and Rothstein calculated that fee lock discouraged 660,000 strikes in 2023, a deadweight loss to the economic system of $17 billion that 12 months.

Mortgage Lock-In Reduces Labor Mobility

Because the property market locks up, labor mobility does, too. Somebody who purchased a typical house at a typical fee in 2016 (3.5 p.c) would pay nearly 40 p.c extra every month, in the event that they have been to take out a contemporary mortgage on an similar house on the now-common fee of round 7 p.c. One research positioned the annual enhance in mortgage funds at $5,000 when transferring to a roughly equal new house, however given the rising value of houses and property taxes, that’s seemingly conservative.

Researchers Julia Fonseca and Lu Liu report, “mortgage lock-in modulates the geographical allocation of labor and results in a mismatch between staff and jobs, as some households forego higher-paid employment alternatives because of the monetary price imposed by mortgage lock-in.” Locked-in households have been half as more likely to transfer in response to potential wage progress.

The favorable distinction in pay or price of residing should be commensurately bigger to entice somebody to grab her potential by transferring to a brand new metropolis, and even throughout city. One other finger on the scales: locked-in mortgage charges are much less more likely to switch into or out of self-employment, and the provision of work-from-home jobs might also make individuals much less more likely to transfer.

Worldwide Alternate options

Different nations have experimented with methods to alleviate lock-in. In the UK and Canada, many mortgages are transportable, that means you possibly can primarily switch your mortgage phrases from an present property to a brand new one. Individuals, normally, safe a mortgage for a specific property and should begin over, with a brand new rate of interest and reimbursement phrases, to buy a subsequent one. Different worldwide mortgages are assumable, that means you possibly can promote your mortgage, with its favorable low charges, to a purchaser together with the property. Particular person owner-occupants should qualify beneath the unique lending phrases. The place do we discover assumable mortgages in the US? Amongst these issued by the Federal Housing Administration (FHA), the Division of Veterans’ Affairs (VA) and a few Division of Agriculture (USDA) loans.

The complicated net of regulation surrounding home-lending put these choices off limits for many Individuals, or at the very least these shopping for with out the assistance of the federal authorities. The Federal Housing Finance Company, on behalf of Fannie Mae and Freddie Mac, instructed The New York Instances and American Banker earlier this 12 months that transportable mortgage choices “usually are not into account” for most people. The Instances concluded, “Proper now by legislation there’s no method to detach that mortgage from the property that serves as its collateral and reattach it to a brand new property.”

Speedy modifications in mortgage charges trigger householders to remain put, and the housing and labor markets undergo the implications. Individuals are much less more likely to transfer, both to larger houses or to higher jobs, stagnating financial mobility. Whereas different nations have discovered artistic, free-market options to cut back the influence of mortgage lock-in, America’s complicated regulatory atmosphere retains these choices out of attain for many patrons.

Portability has its personal peculiarities, like shorter lending phrases and excessive qualification standards. Portability and assumability additionally publish main dangers for buyers who purchase securitized mortgages. Highly effective curiosity teams, together with monetary establishments who at present impose their very own phrases and mortgage brokers who revenue from underwriting and changing every reissued mortgage, additionally play a job in sustaining the established order. Giving Individuals a freer mortgage market with extra selections would possibly profit the economic system, however would take a serious lobbying push.

Mortgage lock-in is only one extra instance of the inevitable, if unintended, penalties of asking the Federal Reserve (or every other group of mortals) to train discretion in these macroeconomic issues. The Federal Reserve has simply minimize the speed by 50 foundation factors and is anticipated to make one other minimize earlier than December, however householders will proceed to really feel locked into their mortgages — and the broader economic system will proceed to really feel the pressure created by current, artificially low charges. Till then, we will anticipate fewer “For Sale” indicators and extra “Keep Put” choices, as monetary incentives prohibit financial mobility.

Laura Williams

Laura Williams is a communication strategist, author, and educator based mostly in Atlanta, GA.

She is a passionate advocate for vital pondering, particular person liberties, and the Oxford Comma.