– Deep Worth “Sum of the components” Particular State of affairs with a Catalyst")

Disclaimer: This isn’t funding Recommendation. By no means belief an nameless dude on the web. DO YOUR OWN RESEARCH!!!

As at all times, I’ve connected a pdf with the total writeup and solely deal with a number of sections on this put up. And the Sound Observe after all.

- Elevator pitch:

Ocean-Wilsons, a UK listed, Bermuda domicile HoldCo which owns a 56% stake in a listed Brazilian Port/Maritime firm referred to as Wilson Sons and an funding portfolio, is buying and selling a a deep low cost (-48%) to its SOTP worth. Now nonetheless it appears very doubtless that the Brazilian Asset shall be offered by yr finish 2024, which may probably set off a re-rating of the inventory on high of any premium paid within the sale.

2. Introduction:

Long term readers of my weblog know that along with investing into boring GARP shares, I additionally make investments into Particular Conditions sometimes. A particular state of affairs is a extra quick time period oriented funding with a transparent set off or catalyst. In earlier instances, I did extra of them, nowadays I’ve much less time and solely look into them in the event that they bounce at me however normally with a comparatively small allocation. There are various kinds of Particular Conditions. This one is of the “Undervalued firm sells main working asset” kind of State of affairs, of which I’ve completed a number of up to now. The final one was Exmar two years in the past with a good end result.

3. Ocean Wilson: Potential sale of main working asset

Ocean Wilsons is a UK listed. Bermuda domiciled holding firm with a market cap of round 470 mn GBP. It’s fairly an uncommon firm. It stories in USD, owns a 57% stake in a listed Brazilian Port/Maritime firm and runs a “fund of fund” hedge fund portfolio.

I got here throughout the corporate through the evaluation of each. Logistec and Eurokai, however didn’t make investments to this point.

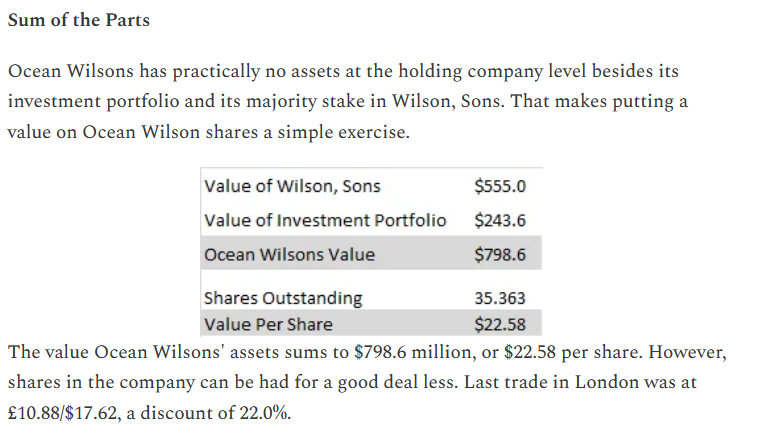

The Steadiness Sheet is difficult to learn because it combines an funding portfolio and the consolidated Brazilian Port operations.

On the plus facet, because the subsidiary is listed, it’s fairly straightforward to see that the worth of that participation referred to as (Wilsons Sons S.A.) is greater than the market cap of the mum or dad firm.

A fast and soiled SOTP evaluation offers us the next Low cost/potential upside:

Previous to the announcement (early June 2023), Ocean Wilsons additionally traded at a 50% low cost, so the low cost to NAV hasn’t narrowed that a lot.

Funnily sufficient, when Alluvial Capital wrote about Ocean Wilson in 2013, the low cost again then was solely 20% (these had been the times….):

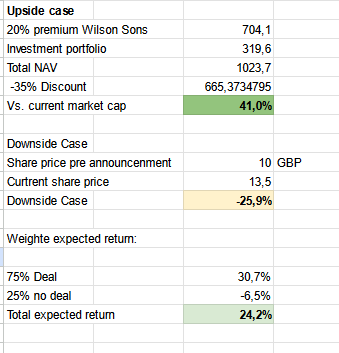

8. Calculation of the potential return:

With a view to calculate a possible return on this particular state of affairs, we have to make a number of assumptions:

- What’s the assumed likelihood of a deal vs. no-deal ?

- What’s the timeline ?

- What would be the final buy worth for the Brazilian stake ?

- What is going to Ocean Wilson do with the proceeds ?

- How will the share worth of Ocean Wilson react, i.e. how would be the low cost to NAV after a deal ?

- What occurs if the deal doesn’t undergo ?

My “intestine feeling” assumptions could be as follows:

- 75% likelihood

- 12 months finish 2024 (for deal announcement, Q1 2025 for NAV low cost tightening)

- Present market worth +20%

- Reinvest in Hedge-Funds

- NAV low cost will slender to -35%

- Share worth will drop again to mid June Degree 2023

This provides us the next “anticipated” return:

After all my assumptions may become fallacious

- The acquisition worth may very well be decrease or greater.

- Perhaps the NAV low cost doesn’t slender in any respect (detrimental).

- Perhaps Ocean Wilson pays a particular dividend and even buys again inventory (optimistic).

- If the deal fails, the share worth may go decrease (detrimental).

- the timeline may very well be additional prolonged

On steadiness, I do suppose that my assumptions usually are not aggressive and ought to be thought of a “Base case”. For me, +24% anticipated return for a possible holding interval of ~6 months seems fairly OK.

11. Conclusion & Recreation Plan:

Ocean Wilsons Holdings seems like a probably fascinating particular state of affairs. There’s a comparatively clear catalyst with first rate upside and the potential draw back seems restricted.

I due to this fact determined to allocate ~2% of the portfolio into this Particular State of affairs funding at ~13,70 GBP/share.

The fascinating half shall be if and after we get additional info on a sale. Equally fascinating shall be if Administration then says one thing about what they’re going to do with the proceeds. Within the Exmar case as an example, there was a time lag between the announcement of the sale and the announcement of a relatively small particular dividend.

It may additionally be useful to observe what Hansa Funding and Wilson Sons will talk in parallel.

Bonus Soundtrack: Mas que nada

Sergio Mendes feat. Black Eyed Peas – Mas Que Nada