Yves right here. Confirming Wolf’s account of the response to the unexpectedly sturdy new jobs report and labor knowledge revisions, the foreign money market has reacted as if the Fed charge cuts are off the desk for now. Rising market currencies fell markedly.

By Wolf Richter, editor of Wolf Road. Initially revealed at Wolf Road

Pandemic distortions and thousands and thousands of migrants all of a sudden getting into the labor market, who’re exhausting to trace, have wreaked havoc on labor-market knowledge accuracy.

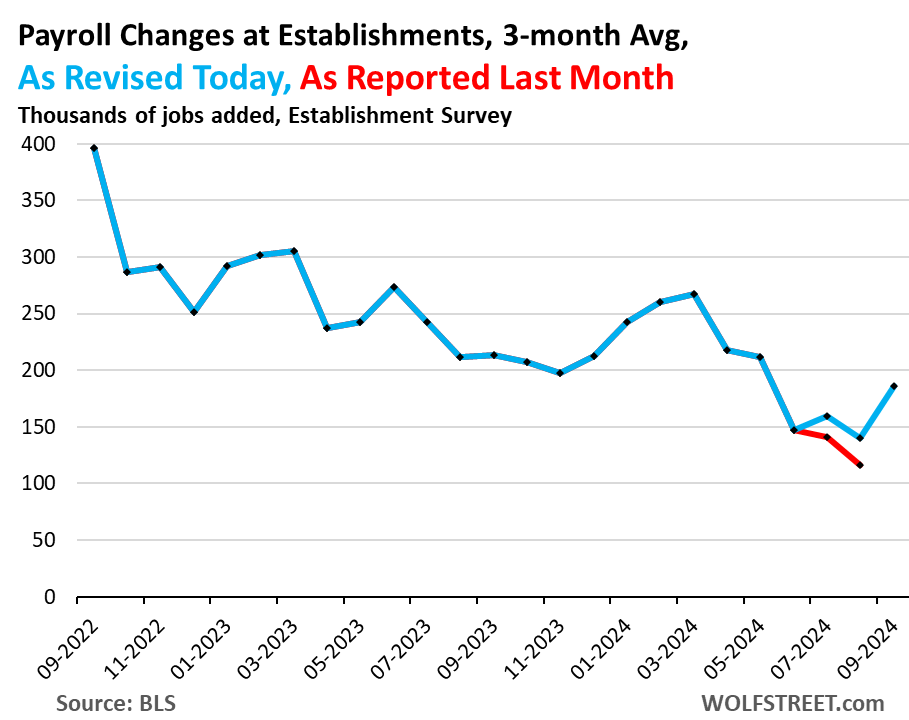

Payrolls at employers rose by 254,000 jobs in September, and the down-revision final month for July was re-revised up so much, and August was revised greater too, so the three-month common jumped to 186,000 payroll jobs created in September. And the three-month common for August – which had been reported as 116,000 on the time, a scary and sudden deterioration with the revisions that precipitated a lot consternation – was revised as much as a half-way first rate 140,000.

Seems, the sudden deterioration of the prior two months have been a false alarm. The labor market is simply superb, creating a good however not spectacular variety of new jobs, and the unemployment charge dropped for the second month in a row, and wages jumped, and the Fed doesn’t want to chop any additional, given the inflation pressures already increase once more — although it’ll seemingly minimize additional, although possibly at a slower tempo than beforehand anticipated.

The blue line exhibits the three-month common of jobs created as reported as we speak. The purple phase exhibits the three-month common as reported a month in the past:

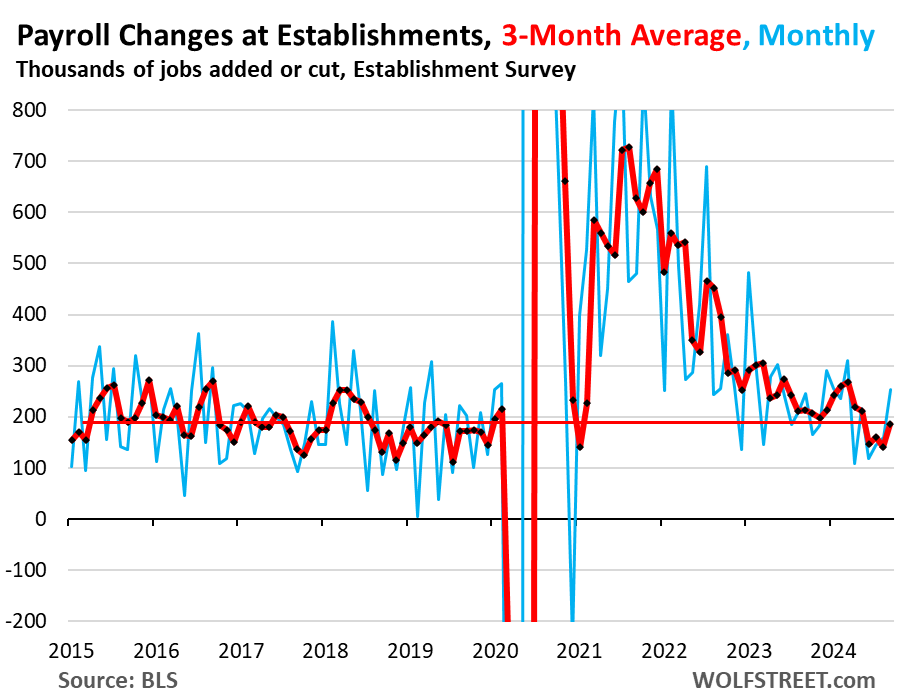

Right here is the lengthy view, as revised: The three-month common is correct within the sweet-spot of the sturdy labor market in 2018 and 2019.

Clearly, the frenetic tempo of hiring after the pandemic is over, and the labor shortages are over. The tempo is again to a wholesome sturdy job development.

This image matches different knowledge exhibiting that layoffs and discharges stay very low. Firms in mixture are creating jobs at a good tempo, they usually’re hanging on to the staff they’ve acquired.

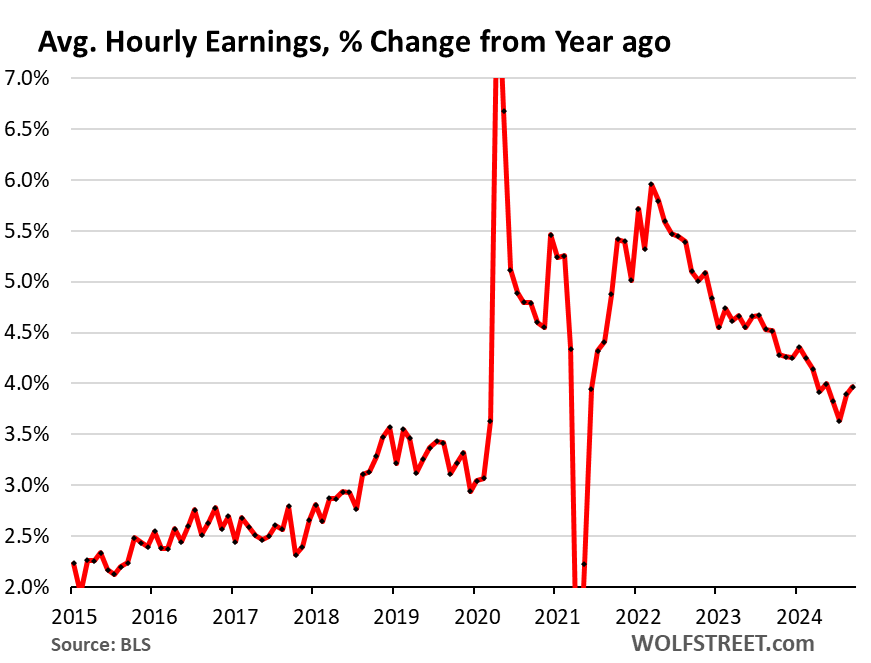

Common hourly earnings have been additionally revised greater for August to a sizzling 5.6% month-to-month annualized, from 4.9%. And in September, they elevated by one other 4.5% annualized from the upwardly revised August, which precipitated the three-month common to extend by 4.3%, the best since January. The three-month common has been rising steadily since April (purple line). That is based mostly on the survey of institutions.

The 12-month enhance of common hourly earnings rose to 4.0% in September, and August was revised greater to three.9% (from 3.8% as reported a month in the past). These two months mixed present the quickest acceleration since March 2022, and are effectively above the peaks of the 2017-2019 interval.

So by way of inflation – and what the Fed has been worrying about – this accelerating wage development will not be entering into the best course anymore.

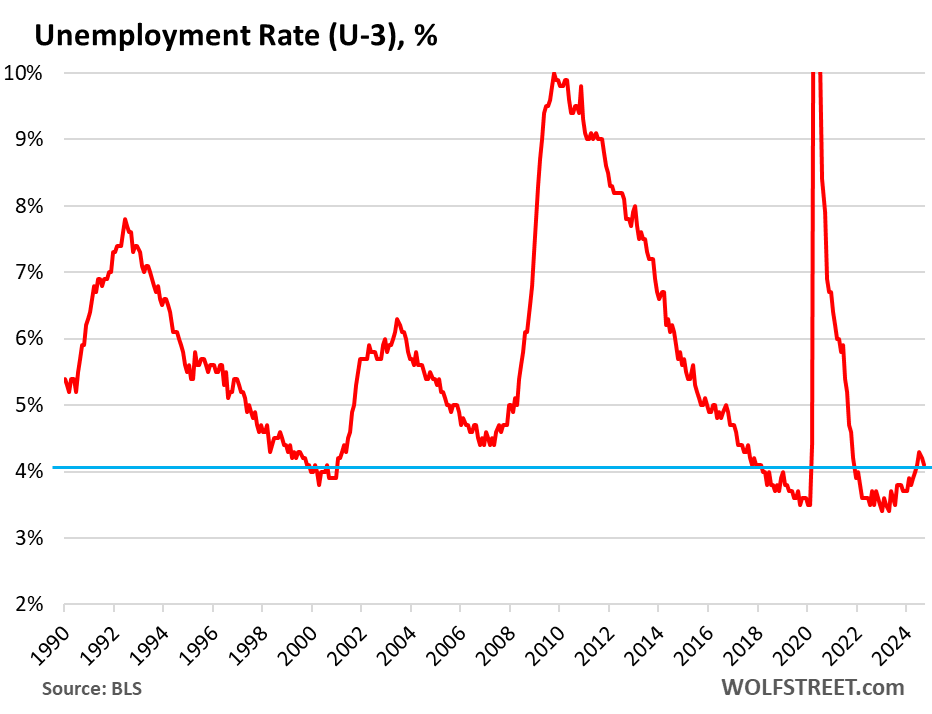

The headline unemployment charge (U-3) dipped to 4.1%, the second month in a row of declines. 4.1% is traditionally low, however is up from the interval of the labor shortages in 2022. That is based mostly on the survey of households.

The unemployment charge is now beneath the Fed’s 4.4% median projection for the tip of 2024 and for the tip of 2025, in accordance with the Fed’s Abstract of Financial Projections launched on the rate-cut assembly.

The weakening of the labor market that the Fed projected in justifying the 50-basis level minimize has reversed, been revised away, or did not occur.

The unemployment charge can also be the place the large inflow of immigrants over the previous two years – estimated at 6 million in 2022 and 2023 by the Congressional Price range Workplace – exhibits up: These which can be in search of a job however haven’t but discovered a job depend as unemployed. And their inflow into the labor pressure has precipitated the unemployment charge to rise from the lows final 12 months.

An increase of the unemployment charge brought on by a surge within the provide of labor is a unique dynamic than an increase of the unemployment charge brought on by job cuts and a discount in demand for labor, as we might see throughout a recession:

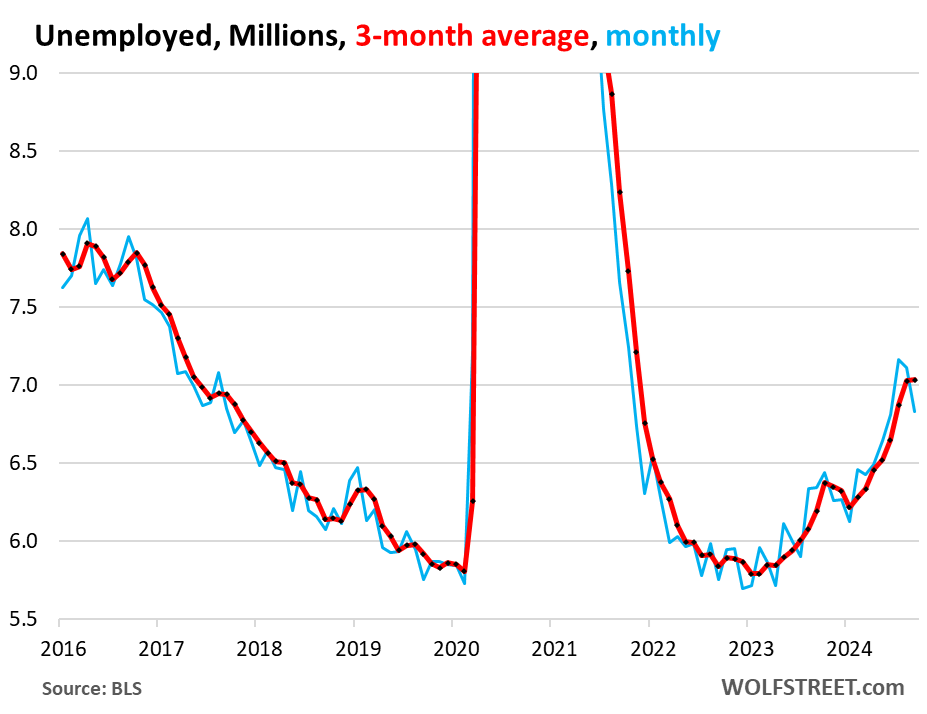

The variety of unemployed individuals in search of a job fell for the second month in a row, to six.83 million. The three-month common inched as much as 7.04 million.

The unemployment charge (chart above) accounts for the large-scale development of the inhabitants and of the labor pressure over the many years. This metric right here of the variety of unemployed doesn’t take note of the expansion of the inhabitants and the labor pressure, and over the many years, a rising inhabitants and labor pressure entails a rising variety of individuals in search of a job.

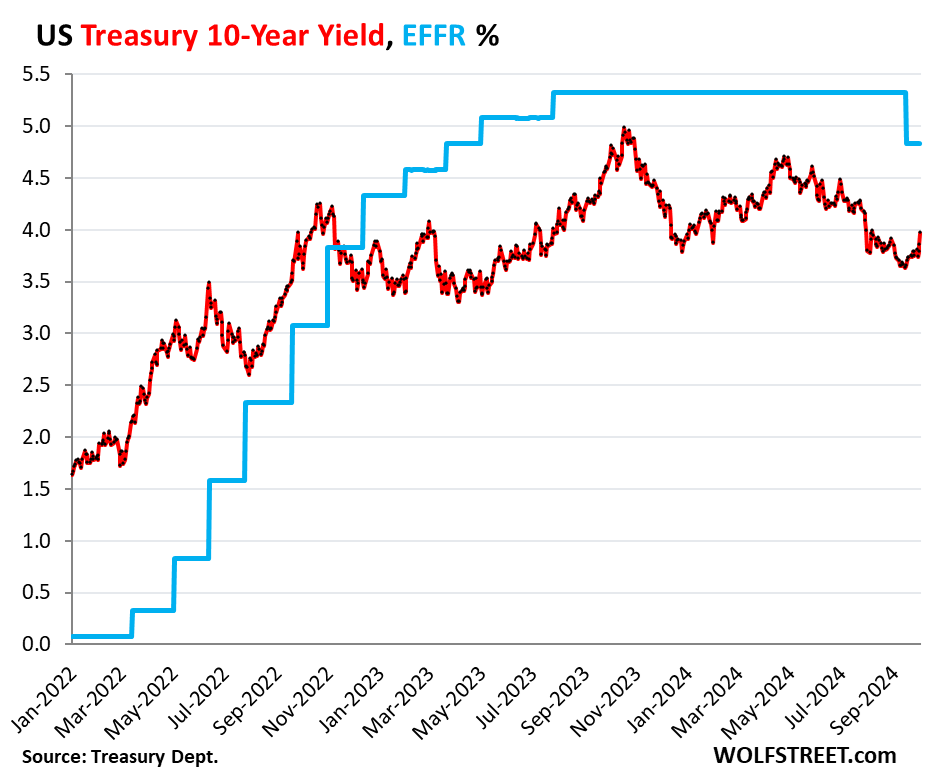

And the bond market wakened.

Upon the information that the labor-market scare final month was a false alarm, and that aggressive charge cuts to avoid wasting the labor market are usually not wanted, and that wage development is contributing to common inflation issues that we’ve got already seen within the Shopper Value Index for August and July, and in what corporations have stated about elevating their costs, and within the pricing energy that corporations nonetheless exert…

Nicely, upon the information, the bond market wakened, and the 10-year yield jumped by 12 foundation factors to three.97% in the mean time, the best since August 8. Because the charge minimize, the 10-year Treasury yield has risen by 27 foundation factors.