DISCLAIMER: This isn’t funding recommendation. The Creator is thought for making a lot of errors in his write-ups and can frontrun you every time doable. DO YOUR OWN RESEARCH !!!!

As at all times in my longer write-up, this put up solely accommodates chosen sections of the write-up- A full pdf is embedded under.

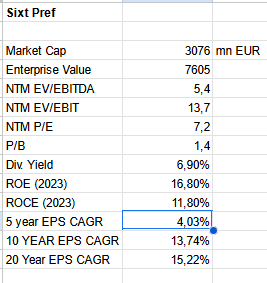

- Administration Abstract

Sixt AG, a family-owned and -run Automotive rental firm from Munich, has been compounding income and shareholder returns at a double digit CAGR for the final 20 years. Following Covid, they accelerated their natural progress within the US which now represents ⅓ of their enterprise and is rising quickly at 20% plus p.a..

As most of their opponents (Hertz, AVIS, Europcar) are overleveraged, they’ll proceed to take market share from them within the coming years. The current (non permanent) points with residual (EV) automotive values depressed valuation multiples in order that Sixt trades at a really low P/E for 2025 (~8 occasions for the Prefs, 11x for the frequent) for what I take into account a top quality firm leading to a beautiful danger return profile.

- Background

Sixt is an organization I owned a number of occasions in my funding profession, sadly by no means lengthy sufficient. Through the preliminary Covid panic, I purchased a “half” place as part of a wider Covid basket” with none deep basic analysis at the moment. Initially, this turned out to be an excellent funding and nearly tripled till the tip of 2021, nonetheless since then, the inventory struggled.

When the Pref Shares hit 50 EUR I tweeted that I couldn’t imagine how low cost the inventory is.

Following that Tweet, I believed it’s a great time to dive a bit of bit extra into the rental automotive trade and see if I ought to “re-underwrite” Sixt or not.

3. Sixt Historical past & some KPIs

3.1. Firm historical past

Sixt was based in 1912 and so technically is the oldest of the massive automotive rental corporations. Nevertheless, solely with Erich Sixt, who turned CEO in 1969, Sixt began to broaden considerably. Sixt went public in 1986 and opened the primary US Department in 2011. In 2021, Erich Sixt after 42 years lastly handed to steer over to his two sons who now run Sixt as Co-CEOs within the 4th era.

3.2. Some KPIs

We will see that over 10 and 20 years (primarily based on 2023), Sixt has been an ideal compounder. Solely during the last 5 years (EPS 2018 adjusted for DriveNow one off acquire), EPS progress slowed. However one has to keep in mind that this time interval features a starting recession (2019), Covid, rate of interest will increase and so forth.

It’s additionally value mentioning that every one that progress was achieved organically. To my data, Sixt by no means acquired one other firm.

Full PDF:

10. Why is the inventory low cost ?

As at all times, when a inventory is reasonable, the query is: Are there any completely good causes for the inventory being so low cost ?

Regardless of the overall weak spot in European small and midcaps, these components would possibly play a task:

- A typical theme I hear is that the rental automotive enterprise is a shitty one. I feel that is primarily as a result of the truth that the issues of AVIS, Hertz and Europcar are very public, however the success of Enterprise isn’t. On a P/E foundation, each Hertz and Avis have traded at comparable multiples (however with much more debt). As Enterprise isn’t publicly traded, some analysts would possibly take a look at Sixt and resolve that it’s even “costly” in comparison with Hertz and Avis.

- Falling residual values for automobiles have impacted Sixt in 2024. Initially, an EBT of 400-520 mn had been forecasted. After Q1, the place they needed to guide a loss due to sudden depreciation, they needed to reduce the steerage once more with the Q2 ends in Could to 350-450 mn EUR. In Q2 as soon as once more they once more diminished the outlook to 340-390 mn EUR. So traders may be afraid that Q3 would possibly include extra damaging surprises.

- Buyers would possibly nonetheless not totally belief the 2 sons to proceed what Erich has achieved over greater than 40 years. I’ve to confess that I’m additionally not 100% satisfied. Solely time will inform.

- Sixt is clearly additionally uncovered to the general financial state of affairs. A deepening recession in Europe would possibly soften the demand, each for trip leases and enterprise clients. Or clients would possibly commerce down from Sixt’s premium provide to a less expensive competitor.

11. Abstract & conclusion

The preliminary query that I requested myself earlier than scripting this put up was: Ought to I re-underwrite Sixt regardless of the fairly disappointing efficiency over the previous months ?

Thea reply after this train for me is clearly YES.

Sixt is a inventory that provides an fascinating progress story, a robust observe document for a really low valuation which in my view creates a really enticing risk-return profile on a mid-term time horizon.

There are clearly some dangers, as talked about my foremost concern is how the sons will carry out as soon as Erich isn’t round anymore.

In any case, I made a decision not solely to “re-underwrite” the inventory however to extend my publicity by shopping for an extra 1% of the portfolio of Widespread shares.

I would add additional, each to the Prefs and the Commons sooner or later if no damaging surprises occur. The date for the discharge of Q3 earnings is November eleventh.